Central Coast Council

Supplementary Business Paper

Extraordinary Council Meeting

01 June 2021

Central Coast Council

Supplementary Business Paper

Extraordinary Council Meeting

01 June 2021

The Extraordinary Council Meeting

of Central Coast Council

will be held Remotely - Online,

on Tuesday 1 June 2021 at 6.30pm,

for the transaction of the business listed below:

2 Reports

2.1 Administrator's Minute - Council’s response to Auditor General’s Local Government Report 4

David Farmer

Chief Executive Officer

AMENDED ITEM

|

Item No: 2.1 |

|

|

Title: Administrator's Minute - Council’s response to Auditor General’s Local Government Report |

|

|

Department: Administrator |

|

|

1 June 2021 Extraordinary Council Meeting |

|

Reference: F2021/00034

- D14664708

Reference: F2021/00034

- D14664708

Author: Rik Hart, Administrator

Recommendation

I formally move:

1 That Council notes the response to the Auditor General’s findings in their Report on Local Government 2020, released on 27 May 2021.

2 That Council supports the recommendation for Office of Local Government to clarify the legal framework relating to restrictions of water, sewerage and drainage funds.

3 That Council commits to implement regular financial reporting, and places on the record future reporting will occur monthly and be presented at Council Meetings and online.

|

|

Background

The Audit Office of New South Wales released its Report on Local Government 2020 on 27 May 2020. The report outlines results of the local government sector council financial statement audits for the year ended 30 June 2020.

Unqualified audit opinions were issued for 127 councils, 9 county councils and 13 joint organisation audits in 2019-20. A qualified audit opinion was issued for Central Coast Council.

Councils were impacted by recent emergency events, including bushfires and the COVID-19 pandemic. The financial implications from these events varied across councils. Councils adapted systems, processes and controls to enable staff to work flexibly.

Auditor General’s Report Highlights for Central Coast Council

A qualified opinion was issued for Central Coast Council (the Council) relating to two matters:

· Council did not conduct the required revaluation to support the valuation of roads.

· Council disclosed a prior period error relating to restrictions of monies collected for its water, sewer, and drainage operations. Based on the NSW Crown Solicitor’s advice, that treatment should be considered a change to a voluntary accounting policy, rather than a prior period error.

Considering the above, the Auditor General made the following recommendation:

The Office of Local Government should clarify the legal framework relating to restrictions of water, sewerage and drainage funds (restricted reserves) by either seeking an amendment to the relevant legislation or by issuing a policy instrument to remove ambiguity from the current framework.

Council’s Response

It is my view that Council should take the opportunity to place on the record its response to the two matters raised in the Auditor General’s qualified opinion.

There is no question Central Coast Council deserves a qualified report given our current financial situation. However, the Auditor Office, in its report made some factually incorrect statements and assumptions that in my opinion require correction and further context.

Revaluation

Council conducted an internal, desktop assessment of roads, bridges and footpaths to determine whether there had been any significant changes in fair value since the last formal revaluation as at 30 June 2015. This assessment was submitted to the Audit Office however they were not satisfied with the methodology that Council used. As a result, Council has commissioned formal external revaluation of its roads, bridges and footpaths to be included in the 30 June 2021 financial statements.

Restricted Funds

Up until the Council merger in May 2016, both Gosford City Council and Wyong Shire Council (who were both water authorities under the Water Management Act 2000) had historically accounted for unrestricted water and sewer cash as restricted as per the Local Government Act 1993.

Upon merger, the above accounting treatment was changed by creating a voluntary accounting policy reported in the 12 May 2016 financial statements for both Councils. This change was not supported by a formal accounting position paper or a legal opinion. In 2017 the audit of the merged entity was taken up by the Auditor General and this voluntary policy accounting treatment was continued but no legal opinion was sought until Council requested a formal legal opinion in December 2020. This was then followed by the Auditor General obtaining a Crown Solicitor opinion in February 2021.

It is important to note that the change in voluntary policy treatment upon merger amounted to a reclassification of over $88 million of water and sewer funds as unrestricted cash for council. This appears to be a material change to be made without a formal accounting position paper or legal opinion.

The notes to the 2016 financial statements identified that the result of the voluntary change in accounting policy was to improve the unrestricted current ratio, which is a key ratio determining whether the merged councils were ‘Fit for the Future’.

Governance

Council detailed to the Audit Office that the voluntary accounting policy that led to the use of externally restricted water and sewer funds was not subject to rigorous internal diligence and did not rest on legal advice (whether internal or external).

There is no evidence that Council ‘argued’ for the change in accounting policy. For that reason, Council is surprised that, when taking over in 2017, the Audit Office did not more heavily scrutinise the governance decisions that underpinned that earlier decision of Council. Particularly since the audit opinion for 2016 offered a disclaimer of opinion because there was insufficient appropriate audit evidence to provide a basis for an audit opinion.

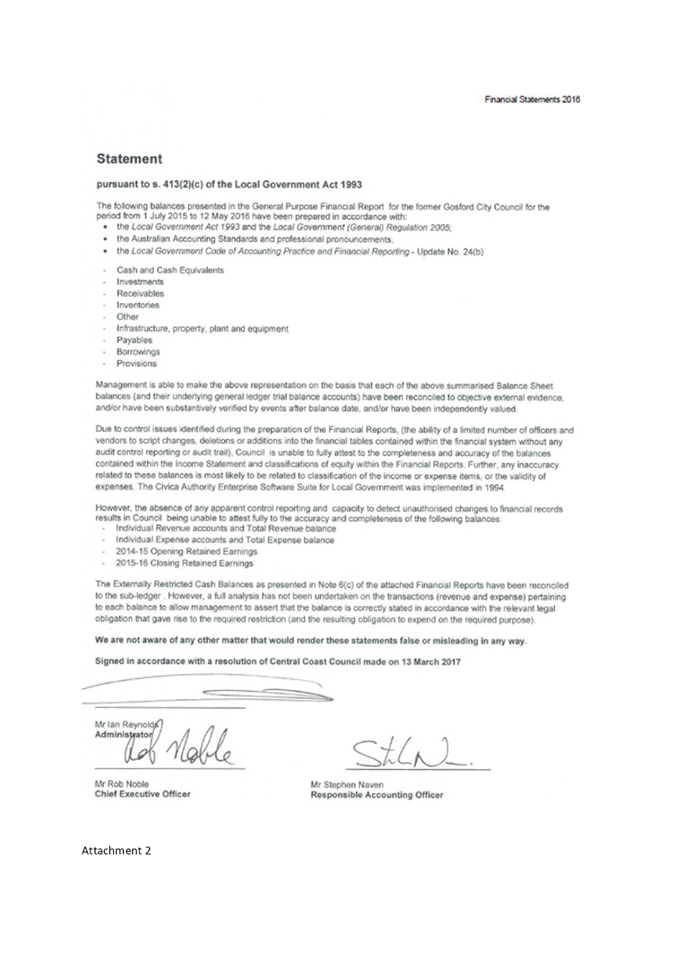

Furthermore as reported in the statement by management in the 2016 Financial Statements, Council’s then CEO Rob Noble and responsible accounting officer Stephen Naven, were unable to fully attest to the completeness and accuracy of the balances contained within the income statement and classifications of equity within the financial reports. Moreover, a full analysis of externally restricted cash balances had not been undertaken to allow management to assert that the balance is correctly stated in accordance with the relevant legal obligation that gave rise to the required restriction.

Council has no record that a position paper supporting any change to the accounting policy was prepared or considered. Any such change to an accounting practice ordinarily requires Council and senior staff (Chief Financial Officer) to sign off, and this did not occur. The Chief Executive Officer at the time has confirmed to me that he was totally unaware of any such accounting policy had been put in place.

I am surprised that the Auditor General or the Audit Risk Improvement Committee (ARIC) did not pick this up, noting it occurred for four consecutive years.

Legal Professional Privilege

Council generally takes a conservative approach to the protection of legal professional privilege. However, now that the Audit Office report has been finalised, Council considers it appropriate to release its advice received from Clayton Utz, as a response to the Crown Solicitor’s Office advice obtained by the Audit Office.

It is noteworthy that Clayton Utz does not consider there was any ambiguity to the legislative position, and that there was no legal basis for the accounting policy adopted by Council in relation to the Water and Sewer funds.

Based on this legal advice, and that there was no formal process for them noting the voluntary change policy, Council determined it was a prior period error.

Looking Forward

Until any legislative ambiguity is resolved Council will tie itself to the Clayton Utz advice regarding the treatment of water and sewer funds as restricted.

Office of Local Government has recommended that local councils no longer have to report on their unrestricted cash position, and I believe removing this requirement could result in more councils breaching their use of both internally and externally restricted funds. In my opinion, it would be sensible for all councils to report on a quarterly basis on their unrestricted and internally and externally restricted funds and that the Auditor General, as part of their audit of councils in the future audit the balance of those funds at year end.

The Central Coast Council will be reporting on a monthly basis Profit and Loss Statement and cashflows both via the internet and Council Meetings.

|

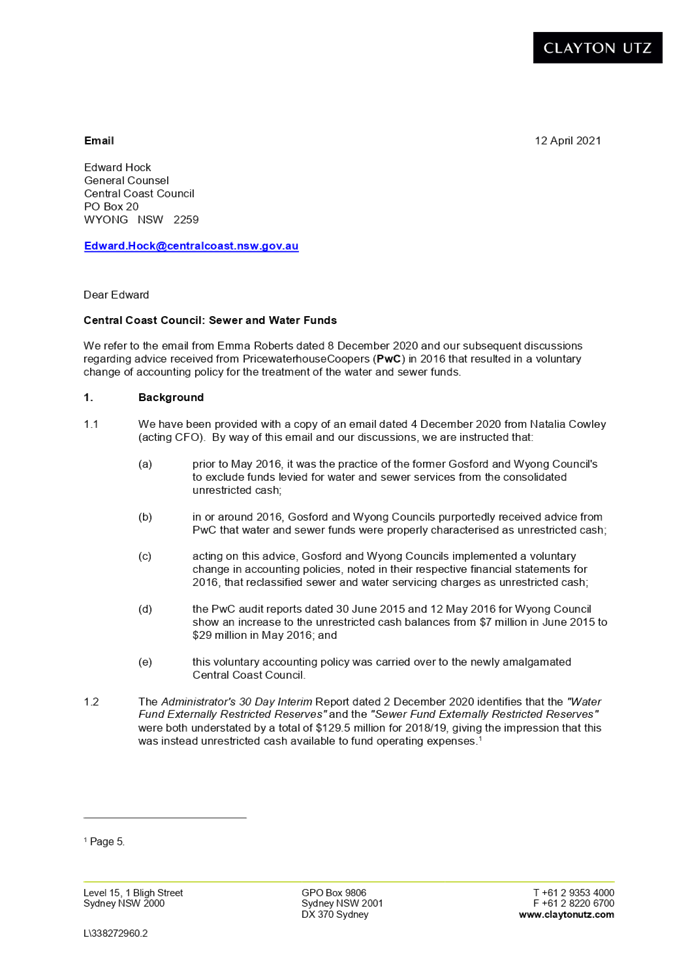

1⇩ |

CU Advice - Letter to E Hock 12.04.21 |

|

D14664631 |

|

2⇩ |

Mr Rob Noble Statement – Financial Statements 2016 |

|

D14664636 |

|

3⇩ |

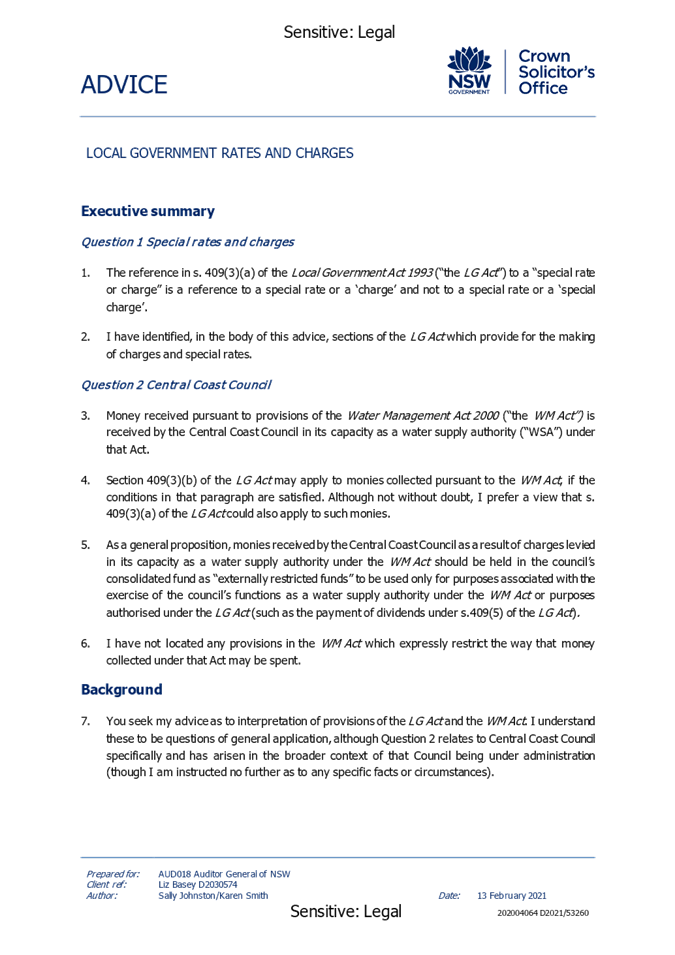

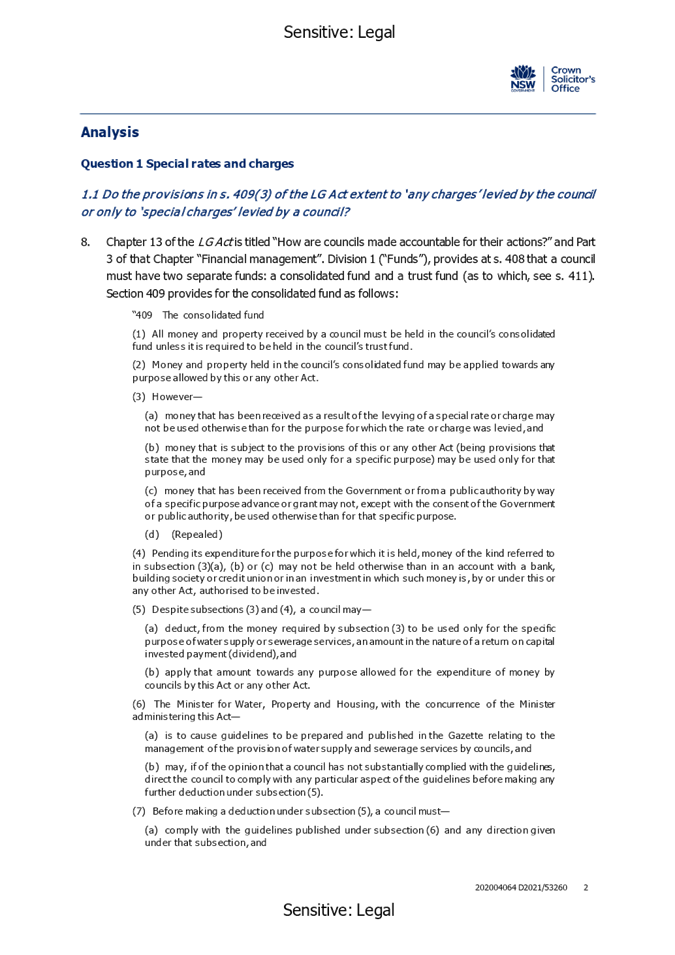

Advice from Crown Solicitor's Office - 13 February 2021 |

|

D14664642 |

|

2.1 |

Administrator's Minute - Council’s response to Auditor General’s Local Government Report |

|

Attachment 1 |

CU Advice - Letter to E Hock 12.04.21 |

|

Administrator's Minute - Council’s response to Auditor General’s Local Government Report |

|

|

Attachment 2 |

Mr Rob Noble Statement – Financial Statements 2016 |